House prices in Canada’s popular ski regions expected to dip 3% over the next year, despite year-over-year price gains

Single-family detached home price increased 15.1% in the first 10 months of 2022

- B.C. ski region of Big White posts highest median price gain in single-family detached segment (45.5%) among regions surveyed

- Quebec’s Mont-Tremblant region reports highest median price increase in condominium segment (44.4%) among regions surveyed

- Southern Georgian Bay’s condominium prices record modest increase of 1.3% year-over-year in 2022, following more than 50% jump last year

- 75% of U.S. border state citizens who own a Canadian recreational property transacted following the federal government’s announcement of a two-year foreign buyer ban

According to the Royal LePage Winter Recreational Property Report released today, Canada’s popular ski regions have posted double-digit year-over-year home price appreciation[1] since the beginning of 2022, despite rising interest rates and price declines in the residential market. Nationally, in the first 10 months of the year, the median price of a single-family detached home increased 15.1% year-over-year to $1,042,700.

“While the rapid rise in interest rates, which began in March of this year, has caused many would-be buyers in the residential market to move to the sidelines, some recreational property purchasers – most notably in higher-end markets – have demonstrated a greater tolerance to increasing monthly mortgage costs,” said Pauline Aunger, broker of record, Royal LePage Advantage Real Estate. “Additionally, many buyers of secondary properties are able to leverage equity from their primary residence or may not require financing at all.”

All recreational regions surveyed recorded double-digit declines in the number of homes sold during the first 10 months of 2022, compared to the same period last year, when demand for properties reached historical highs. Royal LePage recreational property market experts across the country report more balanced conditions and an increase in inventory, compared to 2021. It is widely anticipated that further price growth is unlikely, as activity levels are expected to continue their decline.

“For most Canadians, owning a recreational property is a nice-to-have lifestyle option,” said Aunger. “In the current economic environment, it is not surprising that sales have declined. With recreational homes in greater supply and most staying on the market longer, those that remain in the market are facing less competition, compared to last year. While activity has moderated from the exuberant levels seen during the pandemic boom, demand for recreational properties remains healthy – both as primary and secondary residences. Even as offices reopen and international travel resumes, buyers with the ability to work remotely continue to permanently relocate into recreational communities in search of better work-life balance and access to the outdoors.”

In its 2022 federal budget released on April 7th, the Government of Canada announced that it will be implementing a two-year ban on non-Canadian citizens and non-permanent residents from purchasing residential property in the country.[2] The ban is slated to come into effect on January 1st, 2023. While vacation homes are expected to be exempt from this restriction, the announcement has had a significant impact on the buying intentions of U.S. citizens.

A recent Royal LePage survey of U.S. citizens living in border states,[3] conducted by Leger, found that 75 per cent of those who currently own a recreational property in Canada said that they made their purchase after the two-year foreign buyer ban was announced. Of those who purchased following the announcement, 77 per cent stated that the potential impacts of the ban on their ability to buy real estate in Canada after January 1st, 2023, influenced their decision to purchase before the end of this year.

Among those surveyed who do not currently own a recreational property in Canada, but plan to make a purchase, 67 per cent said that the current strength of the U.S. dollar has made them more inclined to buy a home north of the border. The primary reasons for wanting to buy a recreational property in Canada are multi-season usability (39%), for retirement purposes (38%), and for investment purposes (37%).

“Canada’s winter recreational regions are a draw for our neighbours to the south who are looking for a place to live and play in the winter months. The strength of the U.S. dollar, investment opportunities and relative affordability of recreational properties have enticed buyers from south of the border. With its world-class skiing resorts and picturesque winter landscapes, Canada will remain a desirable location for recreational buyers from all over the world,” said Aunger.

Royal LePage is forecasting that the median price of a single-family detached home in Canada’s recreational ski regions will decrease 3.0 per cent over the next 12 months to $1,011,451.

Data chart – Royal LePage 2022 Winter Recreational Property Report: rlp.ca/table_2022winterrecreationalreport

Survey chart – 2022 Royal LePage Report on U.S. Recreational Property Buyers in Canada: rlp.ca/us-recreational-buyers-2022survey

REGIONAL SUMMARIES

Quebec

Mont-Tremblant (Mont-Tremblant, Saint-Faustin–Lac-Carré, La Conception)

The median price of a single-family detached home in Mont-Tremblant’s recreational property market for the first 10 months of the year increased 23.5 per cent year-over-year to $500,000, while sales decreased 38.1 per cent. Meanwhile, the median price of a condominium increased 44.4 per cent year-over-year to $475,000. Sales in the condominium segment decreased 47.8 per cent in 2022.

For prospective buyers seeking a property slopeside or at mountain base, the current starting prices are around $1.2 million for a single-family detached home and $650,000 for a condominium.

Paul Dalbec, a chartered real estate broker with Mont-Tremblant Real Estate, a division of Royal LePage, says that the Mont-Tremblant real estate market is in the midst of transitioning from a seller’s market to a buyer’s market, which explains the sharp decline in sales. With interest rates moving higher, many potential buyers have adopted a wait-and-see attitude.

“The current slowdown should help shift the Tremblant housing market back to a more normal sales cycle,” Dalbec says. “I expect that in the coming months, slopeside luxury condos worth between $700,000 and $1 million, and single-family residences valued from $400,000 to $600,000 will be most affected by the price correction, as those properties appreciated much more during the pandemic.”

Dalbac says the announcement by the federal government in its April, 2022, budget speech of a ban on foreign housing investments in Canada may have dampened the spirits of some international buyers looking to purchase properties in Mont-Tremblant.

Royal LePage is forecasting that the median price of a single-family detached home in this region will decline by 10 per cent over the next 12 months.

Mont Saint-Sauveur (Saint-Sauveur, Morin-Heights, Piedmont)

The median price of a single-family detached home in Mont Saint-Sauveur’s recreational property market for the first 10 months of the year increased 19.7 per cent year-over-year to $562,500, compared to the same period in 2021, while sales decreased 32.8 percent. Meanwhile, the median price of a condominium increased 22.4 per cent year-over-year to $382,300. Sales in the condominium segment decreased 32.3 per cent in 2022.

For prospective buyers seeking a property slopeside or at mountain base, the current starting price is around $675,000 for a single-family home, and $395,000 for a condominium.

“The year 2023 should usher in better negotiating conditions between sellers and buyers,” predicts Éric Léger, chartered real estate broker with Royal LePage Humania, adding that sellers in the area have started reducing their asking price when the initial listing fails to attract buyers. “Buyers are showing more confidence, with many more of them making conditional offers – that’s something that had all but disappeared during the pandemic. Although the pandemic boom put many first-time buyers into competitive offer scenarios, the current demand comes from experienced buyers whose purchasing power is less affected by economic ups and downs.”

In the coming months, Léger expects to see a steady increase in supply in the region.

Royal LePage is forecasting that the median price of a single-family detached home in this region will decline 5.0 per cent over the next 12 months.

Val Saint-Côme and Mont Garceau (Saint-Côme, Saint-Donat)

The median price of a single-family detached home in Val Saint-Côme’s and Mont Garceau’s recreational property market for the first 10 months of the year increased 17.9 per cent year-over-year to $435,000, compared to the same period in 2021, while sales dropped 36.3 per cent.

For prospective buyers seeking a property slopeside or at mountain base, the current starting prices are around $450,000 for a single-family detached home, and $300,000 for a condominium, although inventory is low in this segment.

“Properties in Lanaudière remain among the most affordable in Quebec’s ski regions, despite the significant increases of the past two years,” observes Éric Fugère, real estate broker with Royal LePage Habitations. “The current period should bring great opportunities for buyers, but even more importantly, time to choose wisely and negotiate fairly. Inventory is creeping up but remains limited, as potential sellers in the region – many of whom are secondary property owners – are waiting for economic conditions to improve and buyer demand to increase, before putting their homes on the market.”

Fugère emphasizes the importance of dealing with a real estate professional when selling or buying a recreational property, especially in the winter.

Royal LePage is forecasting that the median price of a single-family detached home in this region will decline 12.5 per cent over the next 12 months.

Bromont, Sutton (Sutton, Brome and Lac Brome) and Orford (Orford and Magog)

The recreational property markets in Bromont, Sutton and Orford posted uneven price changes during the first 10 months of the year . During this period, the median price of a single-family detached home in Mount Orford (Orford and Magog) increased 17.8 per cent year-over-year to $470,000. In Bromont and Mont Sutton (Sutton, Brome and Lac-Brome), median prices for single-family homes declined 3.0 per cent and 0.9 per cent, to $586,000 and $548,000 respectively, during the same period. Meanwhile, sales declined 25.3 per cent, 39.2 per cent and 12.7 per cent respectively, in Orford, Bromont and Sutton. During the same period, the median price of a condominium climbed 19.5 per cent year-over-year to $498,500 in Bromont, and 16.9 per cent year-over-year to $291,000 in Orford, while sales were down 12.5 per cent and 27.4 per cent, respectively.

For prospective buyers seeking a property slopeside or at mountain base, starting prices currently range from $650,000 to $950,000 for a single-family home and from $450,000 to $650,000 for a condominium.

“The runaway home price increases we saw in the Eastern Townships between 2020 and the first half of 2022 have resulted in a migration of demand toward less congested and less expensive markets,” explains Véronique Boucher, real estate broker with Royal LePage Au Sommet. “Some real estate markets like Bromont reached record high appreciation, which explains why prices have stabilized this year, to the benefit of other, more affordable areas a bit farther away, like Orford. In the condo market, demand for rental assets has contributed to price growth in recent years in Orford, due to the potential for additional income from short-term rentals, as well as strong resale value.”

Looking ahead to the new year, Boucher expects that price appreciation in 2023 will depend greatly on the number of new listings on the market. If there is more inventory, it could give buyers more leverage for negotiating. Given that interest rates will remain relatively high, prices should continue to taper off for the first half of the year.

Royal LePage is forecasting that the median price of a single-family detached home will decline 5.5 per cent in Bromont, 4.0 per cent in Sutton, and 3.0 per cent in Orford over the next 12 months.

Stoneham/Lac-Beauport (Stoneham-et-Tewkesbury, Lac Delage, St-Gabriel-de-Valcartier, Lac-Beauport) and Mont-Sainte-Anne (Beaupré, Sainte-Anne-de-Beaupré, Saint-Ferréol-les-Neiges, Saint-Joachim)

The median price of a single-family detached home near the ski slopes in Stoneham’s and Lac-Beauport’s recreational property market for the first 10 months of the year increased 15.9 per cent year-over-year to $475,300, while sales slipped 26.5 per cent.

For prospective buyers seeking a property slopeside or at mountain base, the starting price is currently around $700,000 for a single-family home, and $300,000 for a condominium.

The median price of a single-family detached home in Mont Sainte-Anne’s recreational property market for the first 10 months of the year increased 4.1 per cent year-over-year to $286,200, with sales decreasing 26.6 per cent. Meanwhile, the median price of a condominium in the region increased 16.0 per cent year-over-year to $145,000. Condominium sales increased 10.4 per cent during the same period.

For prospective buyers seeking a property slopeside or at mountain base, the starting price is typically $700,000 for a single-family home, and $300,000 for a condominium.

“The runaway growth in recreational property prices over the past two years was bound to come to an end,” says Marc Bonenfant, chartered real estate broker with Royal LePage Inter-Québec. “We’ve entered an adjustment phase in the recreational areas of the Capitale-Nationale region, and we should soon see more balance between supply and demand. That means prices will continue to soften through the rest of this year and well into 2023. We will likely see selling times continue to lengthen, although days on market remain below average for the region over the past decade.”

Royal LePage is forecasting that the median price of a single-family detached home will decline 10.0 per cent in the Stoneham/Lac-Beauport market, and 8.0 per cent in the Mont-Sainte-Anne market over the next 12 months.

Data chart – Royal LePage 2022 Winter Recreational Property Report: rlp.ca/table_2022winterrecreationalreport

Survey chart – 2022 Royal LePage Report on U.S. Recreational Property Buyers in Canada: rlp.ca/us-recreational-buyers-2022survey

Ontario

Southern Georgian Bay (Collingwood/Meaford/Thornbury)

The median price of a single-family detached home in Southern Georgian Bay’s recreational property market for the first 10 months of the year increased 11.3 per cent year-over-year to $890,000. Meanwhile, the median price of a condominium increased 1.3 per cent to $679,000 during the same period; a sharp contrast to 2021, when condominium prices rose more than 50 per cent year-over-year. For those looking to buy a house slopeside or at mountain base, prices typically start at $1,500,000. Total sales were down 27 per cent year-over-year in the region, following historic sales volumes in 2021.

“While the number of homes coming onto the market has increased, we are seeing a notable decline in sales activity. The number of days a property typically stays on the market has risen by about 30 per cent since the beginning of the year, settling back to pre-pandemic levels as the buying boom comes to an end,” said Desmond von Teichman, broker, Royal LePage Locations North. “Still, demand remains strong. We continue to see a number of residents with remote working capabilities permanently relocating to the region from the Greater Golden Horseshoe in search of more affordable real estate and better work-life balance. While this trend has slowed, we don’t imagine that it will end soon.”

The short-term recreational rental market has been under pressure as of late, added von Teichman. With global travel having resumed once again, seasonal rentals face diminishing demand and increasing supply as Canadians choose to vacation abroad. The effects of higher inflation, rising mortgage rates and the increased cost of living have also weakened demand on rentals, as many Canadians cut back on discretionary spending. While there has been a slight decrease in demand for luxury properties compared to 2021, von Teichman added that this segment of the market has outperformed the overall market this year.

“Given its convenient proximity to the GTA, Southern Georgian Bay’s real estate market is largely driven by demand from within Ontario,” said von Teichman. “Urban buyers may be somewhat cushioned from the impacts of rising interest rates here, as funds acquired from selling their properties in high-priced surrounding areas tend to stretch farther and boost their buying power.”

Market activity is largely motivated by local demand from nearby cities. However, Ontario remains a desirable destination for U.S. purchasers. Forty-three per cent of U.S. citizens living in border states who currently own a recreational property in Canada have purchased a home in Ontario. Of those who plan to purchase a recreational property in Canada, 48 per cent say they intend to purchase in the province.

Royal LePage is forecasting that the median price of a single-family detached home in Southern Georgian Bay will increase 5.0 per cent over the next 12 months, as the market continues its return to pre-pandemic seasonal trends.

Data chart – Royal LePage 2022 Winter Recreational Property Report: rlp.ca/table_2022winterrecreationalreport

Survey chart – 2022 Royal LePage Report on U.S. Recreational Property Buyers in Canada: rlp.ca/us-recreational-buyers-2022survey

Alberta

Canmore

The median price of a single-family detached home in Canmore’s recreational property market for the first 10 months of the year increased 23.6 per cent year-over-year to $1,588,900, while the median price of a condominium increased 5.9 per cent to $663,400. Total sales were down 41 per cent year-over-year in the region.

“After a record year in 2021, sales have trended back towards long-range historic norms. We have been in a seller’s market for several years, but have recently begun to show signs that we are edging towards a more balanced market in some segments,” said Brad Hawker, associate broker, Royal LePage Solutions. “Inventory has remained at similar levels this past year, which is still well below typical numbers, putting continued upward pressure on prices. Sellers can be reluctant to list their homes in the region, as there is limited inventory of recreational properties to upgrade into.”

Like many recreational markets, Canmore continues to see buyers with remote working capabilities relocate into the community, Hawker added. Although relocation inquiries have reduced, as offices recall employees back to fully-in-office or hybrid work arrangements, Hawker predicts that the work-from-home option will exist for the foreseeable future, adding pressure to the market alongside increased demand from retirees.

“Many Canmore buyers do not require financing. As a result, rising interest rates are not having as significant an impact on our market, compared to other regions. While I do expect prices to soften over the coming year, declines will be modest,” said Hawker. “The impact of higher borrowing costs on the overall economy, however, is causing some buyers to take a wait-and-see approach. Most buyers in this market have the luxury of time, and are waiting to see how things unfold.”

Royal LePage is forecasting that the median price of a single-family detached home in Canmore will decrease 4.0 per cent over the next 12 months, as sales are expected to return to the 10-year average for the region.

Data chart – Royal LePage 2022 Winter Recreational Property Report: rlp.ca/table_2022winterrecreationalreport

Survey chart – 2022 Royal LePage Report on U.S. Recreational Property Buyers in Canada: rlp.ca/us-recreational-buyers-2022survey

British Columbia

Whistler

The median price of a single-family detached home in Whistler’s recreational property market for the first 10 months of the year increased 14.8 per cent year-over-year to $3,648,200, while the median price of a condominium increased 9.7 per cent to $673,300. For those looking to buy a house or condominium slopeside or at mountain base, prices typically start at $2,000,000 and $600,000, respectively. Total sales were down 35 per cent year-over-year in the region.

“In addition to skiing, summer activities such as biking and golfing – coupled with people’s overall desire to be outdoors in nature – make Whistler a popular year-around recreational destination that attracts both regional and international luxury buyers,” said Frank Ingham, associate broker, Royal LePage Sussex. “Home sales have decreased significantly, compared to the pandemic buying boom. And, demand for properties in the area remains strong, although muted compared to last year. Potential buyers today have more choice and more time to sign a deal, as inventory continues to increase along with the average days on market.”

Whistler, which is exempt from British Columbia’s speculation and vacancy tax, has long been a draw for high-end property buyers from all over the world, including many from Seattle, Washington. Thirty-two per cent of U.S. citizens living in border states who currently own a recreational property in Canada have purchased a home in British Columbia. Of those who plan to purchase a recreational property in Canada, 33 per cent say they intend to purchase in the province.

Royal LePage is forecasting that the median price of a single-family detached home in Whistler will decrease 10.0 per cent over the next 12 months, as sales are expected to continue their downward trend, resulting in a surplus of available supply.

Invermere

The median price of a single-family detached home in Invermere’s recreational property market for the first 10 months of the year increased 4.8 per cent year-over-year to $627,500, while the median price of a condominium increased 22.2 per cent to $275,000. For those looking to buy a house or condominium slopeside or at mountain base, prices typically start at $525,000 and $250,000, respectively. Total sales were down 33 per cent year-over-year in the region.

“Invermere is beginning to shift from a strong seller’s market towards a more balanced one. Desirable properties that are well-priced continue to sell quickly, but we are not seeing the same level of demand that we did in 2021. The decline in sales volume directly correlates with the rise in interest rates this year,” said Barry Benson, broker, Royal LePage Rockies West Realty. “Although we have not seen a meaningful rise in resale listings this year, the number of recreational properties available for short-term lease has increased, as many homeowners look to the rental market as a revenue source to offset rising borrowing expenses.”

Over the last year, buyer demand from young couples and retirees in search of affordable housing and a higher quality of life has remained stable. Invermere’s proximity to Calgary makes it an especially attractive option for Alberta buyers who are looking for greater work-life balance, Benson added. While Invermere will continue to see demand for recreational homes and short-term rental properties that offer access to year-round leisure, sales volumes are expected to trend back down to pre-pandemic levels over the next year, from historic highs in 2021, resulting in lower home prices. Low inventory levels will assist in keeping the market competitive and preventing large price reductions.

Royal LePage is forecasting that the median price of a single-family detached home in Invermere will decrease 7.5 per cent over the next 12 months.

Revelstoke

The median price of a single-family detached home in Revelstoke’s recreational property market for the first 10 months of the year increased 13.3 per cent year-over-year to $850,000, while the median price of a condominium increased 36.6 per cent to $778,500. For those looking to buy a house or condominium slopeside or at mountain base, prices typically start at $5,000,000 and $900,000, respectively. Total sales were down 18 per cent year-over-year in the region.

“Property sales have slowed since hikes to interest rates began earlier this year, with first-time buyers and those with tighter budgets the most affected by rising borrowing costs. Still, this will be the second-best year for Revelstoke on record,” said Don Teuton, broker and owner, Royal LePage Revelstoke. “The market is more balanced compared to last year. Potential buyers find themselves in a much less competitive environment, as demand has dampened. While higher home prices and a shortage of inventory continue to be a challenge, price gains recorded since the start of the pandemic boom are unlikely to be sustained.”

Teuton added that homebuyers from outside the region continue to cash in on their existing properties and relocate to Revelstoke in search of a more balanced lifestyle, including some from other higher-cost recreational communities. Despite the current strength of the U.S. dollar, demand from international buyers has been dampened by pandemic fears and travel restrictions. However, Teuton expects that this trend will reverse in the coming years.

Thirty-two per cent of U.S. citizens living in border states who currently own a recreational property in Canada have purchased a home in British Columbia. Of those who plan to purchase a recreational property in Canada, 33 per cent say they intend to purchase in the province.

Royal LePage is forecasting that the median price of a single-family detached home in Revelstoke will decrease 10.0 per cent over the next 12 months, as further interest rate hikes and continued economic uncertainty are expected.

Mount Washington/Comox Valley

The median price of a single-family detached home in the Mount Washington/Comox Valley region’s recreational property market for the first 10 months of the year decreased 5.6 per cent year-over-year to $850,000, while the median price of a condominium increased 18.8 per cent to $475,000. For those looking to buy a condominium slopeside or at mountain base, prices typically start at $300,000. Total sales were down 71 per cent year-over-year in the region, as a result of record low inventory that has reached near-zero levels over the past six months.

“The sense of urgency has disappeared from Mount Washington/Comox Valley’s housing market, resulting in healthier, more balanced conditions for buyers and sellers,” said Rick Gibson, sales representative, Royal LePage in the Comox Valley. “Home prices have leveled off since the end of June. As leaseholds and cash buyers are common in this market, the region is somewhat sheltered from the impacts of rising interest rates.

“Mount Washington is an all-season destination, where residents can enjoy alpine activities in the winter, and beaches, golf courses and hiking in the summer,” Gibson added. “If inventory were to increase, I expect sales would rise in tandem.”

Gibson added that a lack of convenient transportation options, such as flights to and from adjacent states, prevents many interested U.S. buyers from purchasing in the region.

Royal LePage is forecasting that the median price of a single-family detached home in MountWashington/Comox Valley will increase 8.0 per cent over the next 12 months, as extremely low inventory is expected to put continued upward pressure on prices in 2023.

Sun Peaks

The median price of a single-family detached home in Sun Peaks’ recreational property market for the first 10 months of the year increased 13.0 per cent year-over-year to $1,540,000, while the median price of a condominium increased 26.6 per cent to $504,500. For those looking to buy a house or condominium slopeside or at mountain base, prices typically start at $1,350,000 and $320,000, respectively. Total sales were down 25 per cent year-over-year in the region, which is located outside Kamloops, British Columbia.

“Although year-over-year sales are down and available inventory has decreased slightly, home prices have noticeably climbed this past year. Some of the heat has been taken out of the market compared to the 2021 activity levels, although it remains favourable to home sellers,” said Kyle Panasuk, sales representative, Royal LePage Westwin Realty. “We continue to see a desire for home office space from buyers who can work remotely. The local school, skating rink and access to ski-in, ski-out amenities at Sun Peaks are a draw for many local purchasers, as well as remote workers from outside the region looking to relocate to the community full-time.”

Panasuk added that the short-term recreational rental market has continued to perform well in Sun Peaks. Rising interest rates – which have impacted the buying power of both recreational and principal property buyers – may encourage some homeowners to rent out their properties to recoup some of their monthly expenses.

Royal LePage is forecasting that the median price of a single-family detached home in Sun Peaks will increase 8.0 per cent over the next 12 months.

Big White

The median price of a single-family detached home in Big White’s recreational property market for the first 10 months of the year increased 45.5 per cent year-over-year to $1,600,000, while the median price of a condominium increased 11.1 per cent to $500,000. For those looking to buy a house or condominium slopeside or at mountain base, prices typically start at $900,000 and $400,000, respectively. Total sales were down 33 per cent year-over-year in the region, located outside of Kelowna, British Columbia.

“Transactions at the upper end of the market are largely responsible for the dramatic price increases in the single-family segment, as Big White continues to attract luxury recreational property buyers. However, demand has slowed over the last year as buyers adjust to the rising interest rate environment and sellers feel less urgency to list their properties,” said Andrew Braff, sales representative, Royal LePage Kelowna. “As activity moderates, we are seeing fewer multiple-offer scenarios compared to last year.”

Braff noted that luxury property owners are less impacted by changes in the market, and are more likely to keep their properties in the family long-term, for several generations to enjoy.

In addition to local buyers, the world-renowned ski region attracts demand from across the border and around the globe. However, pandemic travel restrictions over the last two years have forced some international homeowners to visit their recreational properties less frequently.

Thirty-two per cent of U.S. citizens living in border states who currently own a recreational property in Canada have purchased a home in British Columbia. Of those who plan to purchase a recreational property in Canada, 33 per cent say they intend to purchase in the province.

Royal LePage is forecasting that the median price of a single-family detached home in Big White will increase 7.0 per cent over the next 12 months.

Data chart – Royal LePage 2022 Winter Recreational Property Report: rlp.ca/table_2022winterrecreationalreport

Survey chart – 2022 Royal LePage Report on U.S. Recreational Property Buyers in Canada: rlp.ca/us-recreational-buyers-2022survey

Royal LePage Royalty-Free Media Assets:

Royal LePage’s media room contains royalty-free assets, such as images and b-roll, that are free for media use.

- Media room: ca/mediaroom

- Royalty-free assets: ca/media-assets

About the Royal LePage Winter Recreational Property Report

The 2022 Royal LePage Winter Recreational Property Report compiles insights, data and forecasts from 16 popular ski regions. Median price and sales data was compiled and analyzed by Royal LePage for the period between January 1, 2022 and October 31, 2022 and January 1, 2021 and October 31, 2021. Data was sourced through local brokerages and boards in each of the surveyed regions. Data availability is based on a transactional threshold and whether regional data is available using the report’s standard housing types.

About the Leger survey

An online survey of 1506 U.S. citizens over the age of 18 living in border states (Maine, New York, Vermont, Pennsylvania, Michigan, Ohio, Wisconsin, Minnesota, North Dakota, Montana, Washington, New Hampshire, Idaho, Oregon, Massachusetts, Indiana and Illinois) was completed between November 8th to November 14th, 2022, using Leger’s online panel. No margin of error can be associated with a non-probability sample (i.e. a web panel in this case). For comparative purposes, though, a probability sample of 1506 respondents would have a margin of error of +/-2.5% on n=1500.

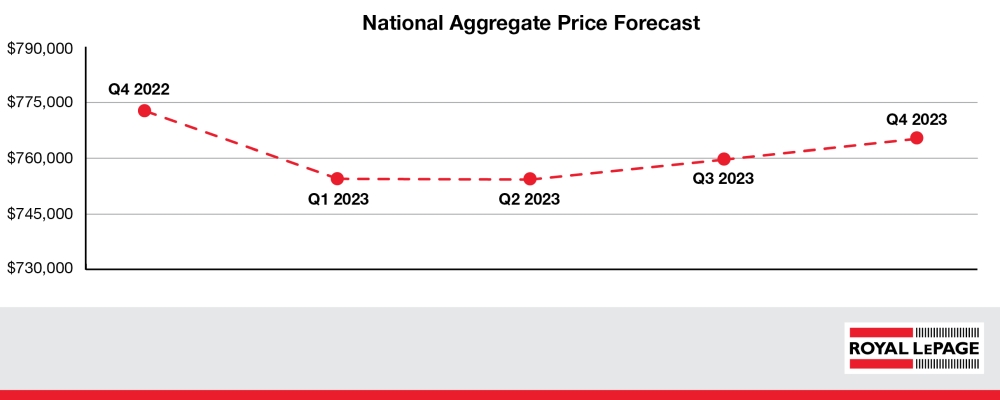

TORONTO, December 13, 2022 – Since the Bank of Canada began raising interest rates aggressively in March of this year, home prices in many major markets across Canada have been decreasing. The rate of decline, however, has been modest. According to the Royal LePage Market Survey Forecast, the aggregate

TORONTO, December 13, 2022 – Since the Bank of Canada began raising interest rates aggressively in March of this year, home prices in many major markets across Canada have been decreasing. The rate of decline, however, has been modest. According to the Royal LePage Market Survey Forecast, the aggregate

If cool concrete dominated Canadian urban architecture between the 1950s and ’80s, and glass and steel typified the 2000s, then mass timber might define the next few decades. Here’s hoping it does. Mass timber is a load-bearing material, usually made of cross-laminated lumber, which is much more cost-effective than concrete or steel. It’s also greener: the wood is renewable and stores CO2. Mass-timber apartment buildings and office towers are currently springing up all over Canada and the world. They include the University of British Columbia’s Brock Commons student residence, the massive Arbora apartment complex in Montreal and George Brown College’s 10-storey Limberlost Place—Ontario’s largest such structure, slated to open in the summer of 2024.

If cool concrete dominated Canadian urban architecture between the 1950s and ’80s, and glass and steel typified the 2000s, then mass timber might define the next few decades. Here’s hoping it does. Mass timber is a load-bearing material, usually made of cross-laminated lumber, which is much more cost-effective than concrete or steel. It’s also greener: the wood is renewable and stores CO2. Mass-timber apartment buildings and office towers are currently springing up all over Canada and the world. They include the University of British Columbia’s Brock Commons student residence, the massive Arbora apartment complex in Montreal and George Brown College’s 10-storey Limberlost Place—Ontario’s largest such structure, slated to open in the summer of 2024. IKEA perfected flat-pack furniture, Casper and Endy the bed-in-a-box. But imagine a whole house that arrives pre-cut and ready to assemble. That’s the promise of the Toronto architectural design firm R-Hauz. The company built, in just seven months, an 18-unit, mass timber building for a transitional-housing shelter in East Gwillimbury, Ontario, and is currently pioneering prefab townhouses. With fixed prices and pre-set design options, they’re designed to come together very fast and appeal to the so-called missing middle of the housing market—buyers who can’t afford a freehold home but don’t want a condo. Modular homes will be popping up across the country in the coming years: such housing is big in B.C. (Click and Nomad Microhomes) and Montreal (Blu Homes, Énergéco).

IKEA perfected flat-pack furniture, Casper and Endy the bed-in-a-box. But imagine a whole house that arrives pre-cut and ready to assemble. That’s the promise of the Toronto architectural design firm R-Hauz. The company built, in just seven months, an 18-unit, mass timber building for a transitional-housing shelter in East Gwillimbury, Ontario, and is currently pioneering prefab townhouses. With fixed prices and pre-set design options, they’re designed to come together very fast and appeal to the so-called missing middle of the housing market—buyers who can’t afford a freehold home but don’t want a condo. Modular homes will be popping up across the country in the coming years: such housing is big in B.C. (Click and Nomad Microhomes) and Montreal (Blu Homes, Énergéco).  9. Toronto’s transportation deficit will deepen

9. Toronto’s transportation deficit will deepen